Introduction to Micro Economics Notes for Class 12 Economics

Please refer to Introduction to Micro Economics Notes for Class 12 Economics provided below. These revision notes have been prepared to help you understand and learn all important topics given in your NCERT Book for Class 12 Economics. We have provided Notes for Class 12 Economics for all chapters provided in your textbooks. These concepts, notes, and solved questions have been prepared for Standard 12 Economics by our expert teachers to help you gain more marks in exams and class tests.

Class 12 Economics Chapter 1 Introduction to Micro Economics Notes

Please carefully read the Introduction to Micro Economics Notes for Class 12 Economics provided below. Use them prior to your exams as this will help you to revise the entire chapter easily. We have also provided MCQ Questions for Class 12 Economics which will be asked in the upcoming exams.

KEY CONCEPTS

- MICRO ECONOMICS

- ECONOMY

- TYPES OF ECONOMY

* PLANNED ECONOMY

* MARKET ECONOMY - CENTRAL PROBLEMS OF AN ECONOMY | BASIC ECONOMIC PROBLEMS

* WHAT TO PRODUCE?

* HOW TO PRODUCE?

* FOR WHOM TO PRODUCE? - CAUSES OF AN ECONOMIC PROBLEM

- PRODUCTION POSSIBILITY CURVE

- MARGINAL OPPORTUNITY COST –MOC

- MARGINAL RATE OF TRANSFORMATION

- SCARCITY OF RESOURCES

- OPPORTUNITY COST

1. MICRO ECONOMICS: It is a study of behaviour of individual units of an economy such as individual consumer, producer etc.

2. ECONOMY: An economy is a system by which people get their living.

3. TYPES OF ECONOMY:

(i) Capitalist economy / Market economy

(ii) Socialist economy / Planned economy

(iii)Mixed economy

4. MARKET ECONOMY: It is an economic system, in which all material means of production are owned and operated by the private with profit motive.

5. PLANNED ECONOMY: In this economy all material means of production are owned by the government or by a centrally planned authority. All important decisions regarding production, exchange and distributions, consumptions of goods and services are made by the government or by a centrally planned authority

6. ECONOMIC PROBLEM: “An economic problem is basically the problem of choice” which arises due to scarcity of resources having alternative uses”.

7. CAUSES OF ECONOMIC PROBLEM :

i) Scarcity of resources

ii) Unlimited wants

iii) Limited resources having alternative uses

8. BASIC (CENTRAL) ECONOMIC PROBLEMS

i). Allocation of resources

a. What to produce?

b. How to produce?

c. For whom to produce

ii). Efficient Utilization of resources

iii). Growth of resources

9. PRODUCTION POSSIBILITY CURVE (PPC): PP curve shows all the possible combination of two goods that can be produced with the help of available resources and technology.

10. MARGINAL OPPORTUNITY COST: MOC of a particular good along PPC is the amount of other good which is sacrificed for production of additional unit of another good.

11. MARGINAL RATE OF TRANSFORMATION: MRT is the ratio of units of one good sacrificed to produce one more unit of other good.

MRT = Unit of one good sacrificed / More unit of other good produced = Δy/Δx

12. SCARCITY OF RESOURCES: Scarcity of resources means shortage of resources in relation to their demand.

13. OPPORTUNITY COST: It is the cost of next best alternative foregone.

14. POSITIVE ECONOMICS: Positive economics deals with what is, what was (or) how an economic problem facing the society is actually solved.

15. NORMATIVE ECONOMICS: It deals with what ought to be (or) how an economic problem should be solved.

VERY SHORT ANSWER QUESTIONS

Question. What do you understand by the problem of how to produce?

Answer : It is the problem of choosing technique of production of goods and services.

Question. What is an economy?

Answer : An economy is a system by which people get their living.

Question. Define marginal rate of transformation.

Answer : MRT is the ratio of units of one good sacrificed to produce one more unit of other goods. MRT = Δy / Δx

Question. What does a rightward shift of PPC indicate?

Answer : It indicates a) growth of resources b) improvement in technology

Question. What do you understand by normative economic analysis?

Answer : Normative economic analysis deals with what ought to be (or) how an economic problem should be solved.

Question. What is economics about?

Answer : Economics is the study of the problem of choice arising out of scarcity of resources having alternative uses.

Question. What do you mean by the problem of what to produce?

Answer : It is the problem of choosing which goods and services should be produced in what quantities.

Question. What is opportunity cost?

Answer : It is the cost of next best alternative foregone.

Question. What is production possibility frontier?

Answer : It is a boundary line which shows the various combinations of two goods which can be produced with the help of given resources and technology.

Question. Give two examples each of micro economics & macroeconomics.

Answer : Microeconomics – Individual demand, individual supply

Macroeconomics – Aggregate demand and aggregate supply

Question. Why PPC is concave to the origin?

Answer : PPC is concave to the origin because of increased marginal opportunity cost.

Question. What is meant by economising of resources?

Answer : It means making best use of available resources.

Question. Name the three central problems of an economy.

Answer : i) What to produce?

ii) How to produce?

iii) For whom to produce?

Question. Define central problem.

Answer : Central problem is concerned with the problems of choice (or) the problem of resource allocation.

Question. What does a point inside the PPC indicate?

Answer : Any point inside the production possibility curve indicate underutilization of resources.

Question. Give one reason which gives rise to economic problems?

Answer : Scarcity of resources which have alternative uses.

Question. What does the problem for whom to produce indicate?

Answer : The problem of for whom to produce refers to the distribution of goods and services produced in the economy.

Question. Define scarcity.

Answer : Scarcity means shortage of resources in relation to their demand is called scarcity.

Question. Why is there a need for economizing of resources?

Answer : Resources are scarce in comparison to their demand, therefore it is necessary to use resources in the best possible manner without wasting it.

Question. What do you understand by positive economic analysis?

Answer : It deals with what is (or) how an economic problem facing an economy is solved. It analyses the cause of effect relationship.

SHORT ANSWER QUESTIONS

Question. Draw a production possibility curve and mark the following situations:

a) underutilization of resources

b) full employment of resources

c) growth of resources

Answer : Every point on PP curve like ABCDEF indicates full employment and efficient uses of resources.

Any point below or inside PP curve like G underutilization of resources.

Any point above PP curves like H indicates growth of resources.

Production Possibility Curve And Opportunity Cost

It refers to a curve which shows the various production possibilities that can be produced with given resources and technology.

Production Possibilities

If the economy devotes all its resources to the production of commodity B, it can produce 15 units but then the production of commodity A will be zero. There can be a number of production possibilities of commodity A & B.

If we want to produce more commodity B, we have to reduce the output of commodity A & vice versa.

Shape of PP curve and marginal opportunity cost.

1) PP curve is a downward sloping curve.

In a full employment economy, more of one goods can be obtained only by giving up the production of other goods. It is not possible to increase the production of both of them with the given resources.

2) The shape of the production possibility curve is concave to the origin.

The opportunity cost for a commodity is the amount of other commodity that has been foregone in order to produce the first.

The marginal opportunity cost of a particular good along the PPC is defined as the amount sacrificed of the other good per unit increase in the production of the good in question.

Example: Suppose a doctor having a private clinic in Delhi is earning Rs. 5lakhs annually.

There are two other alternatives for him.

1) Joining a Govt. hospital in Bangalore earning Rs. 4 lakhs annually.

2) Opening a clinic in his home town in Mysore and earning 3 lakhs annually.

The opportunity cost will be joining Govt. hospital in Bangalore.

Increasing marginal opportunity cost implies that PPC is concave.

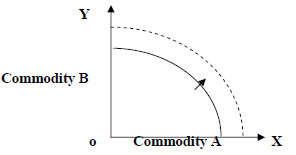

Shift in PP curve

(1) Upward shift

(a) When there is improvement in technology.

(b) Increase in resources.

(2) Downward shift

When Resources depletes

Question. Distinguish between micro economics and macroeconomics.

Answer :

Question. What is production possibility frontier?

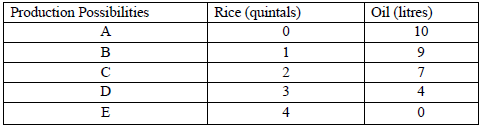

Answer : It is a boundary line which shows that maximum combination of two goods which can be produced with the help of given resources and technology at a given period of time.

Ex: An economy can produce two goods say rice or oil by using all its resources. The different combination of rice and oil are as follows:

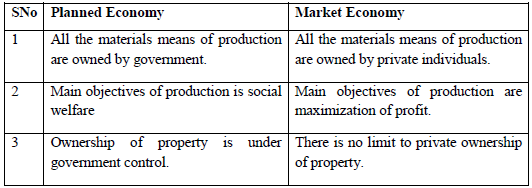

Question. Distinguish between a centrally planned economy and a market economy.

Answer :

Hots Questions

Question. What does the slope of PPC show?

Answer : The slope of PPC indicates the increasing marginal opportunity cost.

Question. Does massive unemployment shift the PPC to the left?

Answer : Massive unemployment will shift the PPC to the left because labour force remains underutilized. The economy will produce inside the PPC indicating underutilization of resources.

Question. How are fundamental problems solved in the planned economy?

Answer : In a planned economy all the economic decisions regarding what, how and for whom to produce are solved by the state through planning. Economic planning replaces the price mechanism. The market is regulated by the state. The prices of the various products are fixed by the state called administered prices.

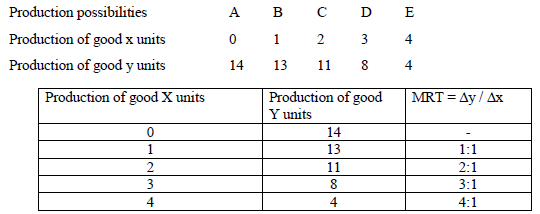

Question. From the following PP schedule calculate MRT of good x.

Question. How are fundamental problems solved in the capitalistic economy.

Answer : In a market-oriented or capitalist economy, the fundamental problems are solved by the market mechanism. Price is influenced by the market forces of demand and supply. These forces help to decide what, how and for whom to produce.